Why a Secured Credit Card Singapore Is Essential for Structure Your Credit Report

Why a Secured Credit Card Singapore Is Essential for Structure Your Credit Report

Blog Article

Exploring Options: Can Former Bankrupts Secure Credit Score Cards Adhering To Discharge?

Navigating the monetary landscape post-bankruptcy can be a challenging job for people looking to rebuild their credit scores. One usual question that develops is whether previous bankrupts can efficiently obtain credit report cards after their discharge. The solution to this query entails a complex exploration of various elements, from credit card choices tailored to this market to the effect of past financial decisions on future creditworthiness. By understanding the details of this process, people can make educated choices that might lead the way for a more protected monetary future.

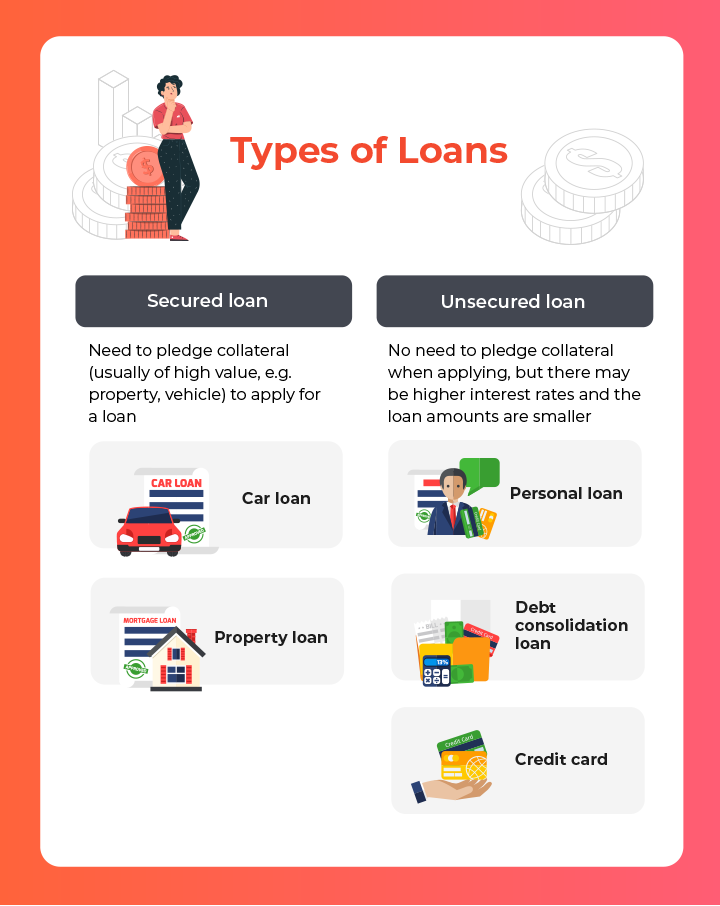

Understanding Debt Card Options

Navigating the world of charge card options calls for a keen understanding of the differing features and terms offered to customers. When taking into consideration bank card post-bankruptcy, people need to meticulously examine their demands and economic circumstance to choose the most appropriate alternative - secured credit card singapore. Protected bank card, as an example, require a cash down payment as collateral, making them a sensible choice for those wanting to restore their credit report background. On the various other hand, unprotected bank card do not necessitate a deposit however may feature greater rates of interest and fees.

Additionally, individuals should pay close focus to the yearly percent rate (APR), grace period, annual costs, and rewards programs used by various credit scores cards. By thoroughly assessing these elements, people can make educated choices when selecting a credit rating card that aligns with their financial goals and circumstances.

Elements Affecting Approval

When applying for credit report cards post-bankruptcy, recognizing the aspects that influence authorization is vital for individuals looking for to reconstruct their financial standing. Complying with an insolvency, debt ratings frequently take a hit, making it tougher to certify for traditional credit score cards. Showing liable financial actions post-bankruptcy, such as paying expenses on time and keeping credit rating use low, can also favorably influence debt card authorization.

Guaranteed Vs. Unsecured Cards

Comprehending the differences in between unsafe and guaranteed credit scores cards is critical for people post-bankruptcy seeking to make educated decisions on restoring their economic health and wellness. Guaranteed credit rating cards call for a money down payment as security, typically equivalent to the credit line expanded by the provider. This down payment minimizes the danger for the bank card company, making it a sensible choice for those with a history of insolvency or inadequate credit score. Safe cards typically include reduced credit line and greater rate of interest compared to unsecured cards. On the other hand, unsecured charge card do not require a cash down payment and are based only on the cardholder's credit reliability. These cards normally supply greater credit line and reduced passion prices for individuals with great credit history. However, post-bankruptcy individuals may discover it challenging to get unsafe cards promptly after discharge, making secured cards an extra feasible alternative to start reconstructing debt. Eventually, the selection between safeguarded and unprotected credit rating cards depends upon the person's this contact form financial circumstance and credit goals.

Structure Credit Scores Sensibly

To effectively reconstruct credit scores post-bankruptcy, developing a pattern of liable credit scores use is crucial. One key way to do this is by making timely repayments on all charge account. Payment history is a considerable aspect in establishing credit scores, so ensuring that all bills are paid on schedule can gradually improve creditworthiness. Additionally, keeping charge card equilibriums reduced about the credit line can favorably affect credit rating. secured credit card singapore. Professionals advise maintaining debt usage below 30% to demonstrate liable credit monitoring.

Another technique for developing credit rating responsibly is to keep track of credit score reports regularly. By evaluating credit history records for errors or indications of identity theft, individuals can deal with problems quickly and preserve the precision of their credit history.

Gaining Long-Term Conveniences

Having developed a foundation of responsible credit rating management post-bankruptcy, people can now focus on leveraging their boosted credit reliability for long-lasting financial advantages. By regularly making on-time payments, maintaining credit report usage low, and checking their credit score reports for accuracy, previous bankrupts my sources can gradually restore their credit history. As their credit rating enhance, they may come to be qualified for far better credit scores card uses with lower passion rates and greater credit line.

Enjoying long-term take advantage of boosted creditworthiness prolongs past just charge card. It opens doors to desirable terms on fundings, home mortgages, and insurance policy premiums. Full Report With a strong credit report, people can work out much better passion rates on finances, possibly saving countless bucks in interest repayments gradually. In addition, a positive credit history account can boost job prospects, as some employers might inspect credit reports as part of the hiring process.

Conclusion

To conclude, previous insolvent people may have difficulty protecting bank card complying with discharge, yet there are alternatives available to help reconstruct credit score. Recognizing the various types of charge card, aspects influencing authorization, and the relevance of liable bank card use can aid people in this scenario. By picking the appropriate card and utilizing it properly, previous bankrupts can slowly enhance their credit report and enjoy the long-lasting advantages of having accessibility to debt.

Showing accountable monetary habits post-bankruptcy, such as paying bills on time and maintaining credit utilization reduced, can likewise positively influence credit rating card approval. Additionally, maintaining credit history card balances low relative to the credit rating limit can positively affect credit report ratings. By consistently making on-time repayments, maintaining credit history utilization reduced, and monitoring their credit report reports for precision, former bankrupts can slowly restore their credit rating scores. As their credit ratings increase, they may come to be eligible for far better credit score card supplies with lower rate of interest prices and higher credit rating restrictions.

Understanding the various kinds of credit score cards, elements influencing approval, and the value of liable credit report card use can assist people in this situation. secured credit card singapore.

Report this page